DSCR loans make it easier for Airbnb investors to secure financing by focusing on property income rather than personal financial details. Here’s what you need to know:

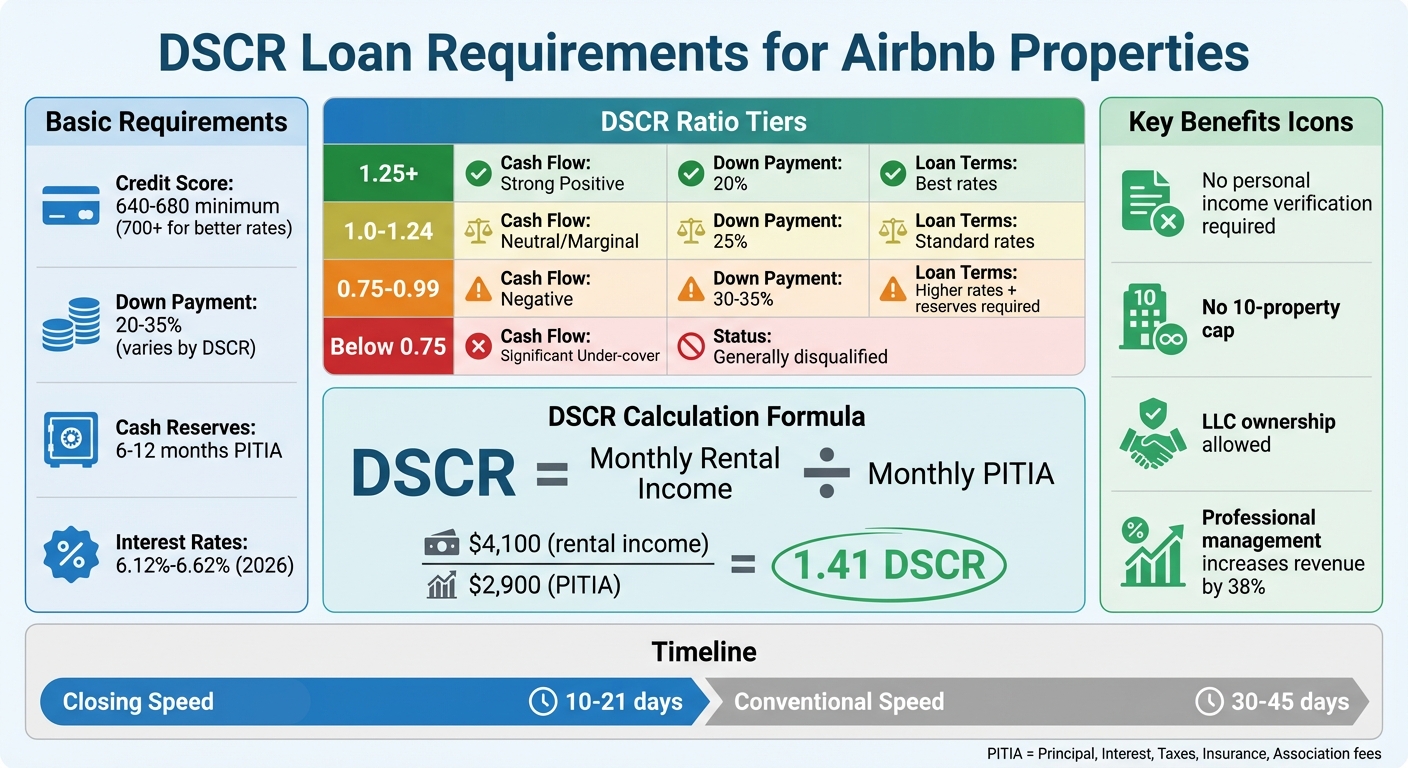

- DSCR Basics: The Debt Service Coverage Ratio (DSCR) measures how well rental income covers a property’s expenses. A DSCR of 1.25 or higher is ideal for better loan terms.

- Airbnb Income: Lenders may use tools like AirDNA or Airbnb booking history to assess income. This is especially helpful for short-term rental investors.

- Down Payment & Credit: Expect a down payment of 20–30% and a credit score of at least 640. Higher scores and DSCRs can lead to better rates.

- Quick Process: DSCR loans often close faster (10–21 days) and allow properties to be titled under LLCs for added flexibility.

- Local Laws Matter: Ensure the property complies with short-term rental regulations and has necessary permits.

DSCR Loan Requirements and Qualification Tiers for Airbnb Properties

How To Qualify for DSCR Loans for Airbnb: Step-by-Step Financing Guide

sbb-itb-103bddb

What Is a DSCR Loan and How Does It Work for Airbnb Investors

A DSCR loan is a type of mortgage specifically designed for investment properties. Instead of focusing on the borrower’s personal financial details, this loan evaluates the property’s rental income to determine eligibility [2][7]. This makes it particularly appealing to Airbnb investors, who often reduce their taxable income through depreciation and other write-offs. Essentially, the loan prioritizes the property’s financial performance over the borrower’s personal financial situation.

As DSCRTool.com puts it:

With a conventional mortgage, the lender asks: ‘Does this person earn enough to afford this payment?’ With a DSCR loan, the lender asks: ‘Does this property earn enough to cover its own payment?’

For Airbnb properties, lenders typically verify income using either a 12-month rental history from platforms like Airbnb or VRBO, or projected revenue from third-party tools such as AirDNA [3][6][8]. This approach allows investors to secure financing for new purchases, even if the property lacks an extensive rental history.

How to Calculate DSCR

The Debt Service Coverage Ratio (DSCR) is calculated by dividing the property’s gross monthly rental income by its total monthly debt payment (PITIA). PITIA includes Principal, Interest, Taxes, Insurance, and any HOA or association fees [2][4][7].

For example, if your Airbnb generates $4,100 per month in rental income and your total PITIA payment is $2,900, your DSCR would be 1.41. This means the property earns 41% more than its debt obligations. While a minimum DSCR of 1.0 is required to break even, a ratio of 1.25 or higher is often considered the "gold standard", offering better interest rates and lower down payment requirements [4][8].

Here’s a quick breakdown of typical DSCR tiers:

| DSCR Ratio | Cash Flow Status | Typical Lender Treatment |

|---|---|---|

| 1.25+ | Strong Positive | Best rates and lowest down payments (around 20% down) |

| 1.0 – 1.24 | Neutral/Marginal | Standard rates with slightly higher down payments (about 25%) |

| 0.75 – 0.99 | Negative | Higher down payments (30–35%) and significant cash reserves required |

| Below 0.75 | Significant Under-cover | Generally disqualified from most standard DSCR programs |

Some lenders now accept DSCR ratios as low as 0.75 to 0.80 if the borrower provides a higher down payment (typically 30–35%) or maintains substantial cash reserves. This can be a game-changer for investors in high-cost markets where properties may not immediately reach a DSCR of 1.25.

Why DSCR Loans Work Well for Airbnb Properties

One of the biggest advantages of DSCR loans is that they don’t require personal income verification. You won’t need to submit tax returns, W-2s, or pay stubs, making them ideal for self-employed investors or those who use aggressive tax strategies.

Another benefit is the ability to scale your portfolio. Since DSCR loans don’t impact your personal debt-to-income ratio, you can acquire multiple properties without worrying about the 10-property cap that comes with conventional loans. Additionally, these loans often allow properties to be titled under an LLC or S-corp, which can provide better asset protection.

The approval process for DSCR loans is also relatively quick, often closing within 21 to 30 days due to simplified documentation. If you’re looking to expand your portfolio in competitive markets like Denver or Pittsburgh, this speed can give you an edge over other buyers. While DSCR loans usually come with interest rates about 0.5% to 1.5% higher than conventional investment loans [4], the flexibility they offer often outweighs the additional cost.

Basic DSCR Loan Qualification Requirements

Knowing the basic criteria that most DSCR lenders use to evaluate Airbnb properties can help you gauge your chances of loan approval and the terms you might receive.

Credit Score and Down Payment

Most lenders require a minimum credit score between 640 and 680 [4]. However, just hitting the minimum won’t necessarily get you favorable terms. Borrowers with credit scores above 700 often secure better interest rates – typically 0.25% to 0.50% lower for every 20-point increase beyond 700 [4]. Some niche lenders may work with scores as low as 620, but these loans generally come with higher rates [3].

Down payment requirements depend on the property’s DSCR (Debt Service Coverage Ratio). Properties with a DSCR of 1.25 or higher usually need a down payment of 20%–25%. Those with a DSCR below 1.25 might require 30%–35% [4]. Additionally, lenders often require borrowers to have 6 to 12 months of PITIA (Principal, Interest, Taxes, Insurance, and Association dues) reserves in accessible accounts like savings or money market funds.

| DSCR Ratio | Cash Flow Status | Typical Down Payment |

|---|---|---|

| 1.25 or higher | Positive (Preferred) | 20%–25% |

| 1.0 – 1.24 | Neutral/Marginal | 25%–30% |

| Below 1.0 | Negative Cash Flow | 30%–35% |

Beyond financial qualifications, the property itself must meet certain compliance standards to secure a DSCR loan.

Property Location and Short-Term Rental Eligibility

Properties located in areas with bans or strict regulations on short-term rentals can pose challenges for DSCR loan approval [9]. It’s essential to check local zoning laws, permits, and HOA rules to confirm the property’s eligibility for short-term rentals. Some markets, such as certain neighborhoods in Denver and Scottsdale, have specific licensing requirements or may cap the number of available permits. In some cases, HOAs might allow rentals with a 30-day minimum stay but prohibit nightly rentals, which could disqualify the property for Airbnb use.

STR (short-term rental) insurance is another requirement. Lenders typically expect at least $100,000 in liability protection along with six months of rent-loss coverage [9].

The type of property also influences approval odds. Single-family residences and condos are generally preferred by DSCR lenders. In contrast, multi-family properties or townhomes often face stricter evaluation or may even be excluded outright [9]. Properties in urban hubs and popular tourist destinations – like Orlando, Gatlinburg, and Lighthouse Point – tend to be easier to finance due to their transparency in occupancy data and steady rental demand [8].

How to Qualify for a DSCR Loan: Step-by-Step Process

Securing a DSCR loan requires careful preparation and thorough documentation. Here’s how to approach the process.

Check Local Laws and Permits

Before you dive into financing, ensure your target property is legally eligible to operate as a short-term rental. This means reviewing your area’s zoning laws, homeowners’ association (HOA) restrictions, and any required permits. Some cities have strict rules, such as limiting the number of short-term rental licenses or requiring specific insurance policies. For example, neighborhoods in cities like Denver and Scottsdale enforce licensing regulations that might impact your investment. Contact your local planning department to confirm what’s needed and whether permits are available.

Calculate Your Property’s DSCR

For properties with an existing rental history, request 12–24 months of booking data from the seller. If you’re eyeing a new investment, platforms like AirDNA, Rabbu, or PriceLabs can provide revenue estimates. These reports are crucial for demonstrating income potential to lenders.

Lenders evaluate income from one of three sources: historical performance, projections from analytics tools, or an appraiser’s Short-Term Rental Schedule. To calculate your DSCR, divide your projected gross rental income by your monthly PITIA (Principal, Interest, Taxes, Insurance, and HOA dues).

Here’s an example: In February 2026, an investor in Austin, Texas purchased a $725,000 property. Using AirDNA, they estimated a $325 nightly rate with 60% occupancy, leading to $5,850 in gross monthly income. With a 20% down payment ($145,000), their monthly PITIA was $4,600, giving them a DSCR of about 1.27. Keep in mind, lenders often apply a 20–25% expense factor for vacancy, cleaning, and maintenance, which can affect the final DSCR calculation.

Once you’ve determined your DSCR, you’re ready to move forward with documentation.

Gather the Necessary Documents

DSCR loans focus on property cash flow rather than your personal income, so traditional documents like W-2s or tax returns aren’t typically required. Instead, you’ll need:

- For existing rentals: Download 12 months of booking history from platforms like Airbnb or VRBO.

- For new purchases: Include income projections from tools like AirDNA to provide market-supported estimates.

You’ll also need 2–3 months of bank statements to show you have enough funds for the down payment and 6–12 months of PITIA reserves in liquid accounts. If you’re purchasing under an LLC (a common preference for DSCR lenders), gather your LLC formation documents, operating agreement, and EIN. Additionally, an STR-specific appraisal (Form 1007) that includes an Alternative STR Market Rental Analysis is essential. This appraisal focuses on daily rates and expected occupancy rather than standard long-term lease data.

Improve Your DSCR by Adjusting Revenue or Expenses

If your DSCR falls below 1.25, there are ways to improve it. Increasing your down payment – often between 25% and 30% for short-term rentals – can lower your loan amount and monthly payments. Alternatively, you could explore interest-only payment options to reduce your mortgage expense.

On the income side, implementing dynamic pricing strategies can help maximize both occupancy and nightly rates. Professional management services can also make a big difference. For instance, property owners working with Rank One Stays see a 38% revenue boost through optimized listings, dynamic pricing, and round-the-clock guest support. This not only strengthens your DSCR but also highlights the property’s potential to lenders, improving your chances of approval.

Choose Lenders That Accept Airbnb Income

Not all DSCR lenders recognize short-term rental income, so it’s essential to find those that specialize in this type of financing. Look for lenders who accept third-party income projections from platforms like AirDNA and explicitly mention STR or Airbnb loans.

When comparing lenders, consider factors like interest rates (which ranged from 6.12% to 6.62% in early 2026 for borrowers with strong ratios), loan-to-value limits, reserve requirements, and LLC vesting options. Some lenders may require 12 months of proven rental performance, while others accept market projections for new properties. Be sure to verify their minimum DSCR thresholds – typically between 1.0 and 1.25 for short-term rentals – and ask if higher ratios can secure better loan terms.

Working with lenders experienced in vacation rental markets, such as those operating in Nashville, Gatlinburg, or Lighthouse Point, can simplify the process. These lenders understand the seasonal income fluctuations and unique challenges of short-term rental properties, making them better equipped to handle your application.

How to Strengthen Your DSCR Loan Application

Improving your DSCR loan application means focusing on strategies that enhance your property’s Debt Service Coverage Ratio (DSCR). A stronger DSCR not only reduces the lender’s risk but also helps you secure better financing terms. By going beyond the basics, you can show lenders that your property is a reliable investment with solid income potential.

Hire Professional Management to Increase Revenue

Teaming up with a professional vacation rental management company can significantly boost your property’s revenue, which directly improves your DSCR. These companies often use dynamic pricing strategies, professional photography, and compelling descriptions to make your property stand out. They also list your property across multiple platforms and provide 24/7 guest support, ensuring maximum occupancy and income.

Lenders often value these services and may accept income reports from property managers or a Form 1007 rent schedule as evidence of projected performance. This can be especially helpful for first-time investors who lack prior experience. Including a copy of your management agreement in your application can reassure lenders that your property will be professionally handled, reducing their perceived risk [1][11].

For example, owners working with Rank One Stays have reported revenue increases of up to 38% thanks to optimized listings, guest support, and strategic pricing. Markets like Denver or Scottsdale can benefit even more from partnering with a local management company that understands the area’s unique rental dynamics.

Beyond professional management, presenting a solid business plan can further validate the income potential of your property.

Create a Detailed Business Plan

A thorough business plan can set you apart by showcasing your understanding of the market and your property’s earning potential.

Start with a market analysis that covers local competition, seasonal demand trends, and your target audience – whether it’s families, business travelers, or remote workers. Include detailed financial projections for nightly rates, occupancy levels, fixed costs, and variable expenses. Tools like AirDNA and Mashvisor can provide data to back up your estimates.

Highlight what makes your property stand out – whether it’s proximity to attractions, modern amenities like high-speed Wi-Fi, or pet-friendly features. Adding measurable goals, key performance indicators (KPIs), and a monthly cash flow forecast can further demonstrate how your property will perform, even during slower seasons.

Provide Proof of Rental Income

With your management strategy and business plan in place, strong income documentation is the next step. Provide 12–24 months of rental history from platforms like Airbnb or Vrbo, along with bank statements that verify consistent income [5].

For newer properties without a rental history, you can use AirDNA reports with a Market Score of 60 or higher and proper expense breakdowns to project income [12]. Alternatively, request a specialized Form 1007 appraisal that focuses on short-term rental data rather than traditional long-term leases [12].

"If the rental income covers – or comes close to covering – the payment, you can often qualify – even when traditional lenders say no." – ABO Capital [2]

Additionally, showing future booking calendars can highlight immediate demand and upcoming cash flow [10]. If an appraisal comes in low, prepare a rebuttal package with updated comparables or additional AirDNA data to strengthen your case [12].

Conclusion

Securing a DSCR loan for your Airbnb property hinges on demonstrating that the property generates enough income to cover its debt. Key steps include calculating your DSCR ratio (aim for 1.25 or higher), providing 12–24 months of rental income records or AirDNA projections, maintaining a credit score of at least 640–680, and preparing a 20–25% down payment. Additionally, you’ll need to confirm that short-term rentals are permitted in your area, set aside 3–12 months of cash reserves, and find lenders who accept Airbnb income.

Improving your property’s revenue is crucial for a strong application. Professional management can help by increasing occupancy rates and fine-tuning nightly pricing – two factors lenders pay close attention to. With interest rates steady between 6.12% and 6.62% as of early 2026, showcasing consistent and professional operations can help you secure better loan terms.

Rank One Stays supports property owners in meeting lender requirements through tools like dynamic pricing, 24/7 guest support, and detailed financial reporting. On average, property owners working with Rank One Stays earn 38% more revenue than the market standard, which strengthens DSCR ratios and improves loan eligibility. Whether you’re investing in Denver, Scottsdale, or other areas, partnering with experienced managers can provide the performance and documentation needed to secure approval.

FAQs

Can I qualify with no Airbnb rental history?

Yes, it’s possible to qualify for a DSCR loan for an Airbnb property even if you don’t have personal rental history. Many lenders prioritize the property’s potential or actual income over your past rental experience. They often rely on tools like projected rental income reports or data from platforms like Airbnb to evaluate the property’s earning potential. To improve your chances, focus on meeting the lender’s other requirements and presenting solid income projections for the property.

What income will lenders count for my Airbnb?

When applying for a DSCR loan for an Airbnb property, lenders focus on the projected rental income from the property rather than your personal income or tax returns. Their main concern is whether the property can generate enough cash flow to cover the mortgage payments. This is determined by calculating the Debt Service Coverage Ratio (DSCR), which is the property’s gross rental income divided by the monthly payment (PITI). A DSCR of at least 1.0 is typically required to qualify.

Can I get a DSCR loan in an LLC?

Yes, you can absolutely obtain a DSCR loan under an LLC. These loans are tailored for financing investment properties owned by entities like LLCs. Instead of evaluating your personal income, lenders primarily assess the cash flow generated by the property. This makes DSCR loans a great option for investors looking to utilize rental income while keeping the property within an LLC structure.