Owning a vacation rental property is more than just an income opportunity – it’s a long-term investment that requires careful planning to ensure smooth transitions across generations. Without a proper succession plan, families risk disputes, financial losses, and heavy tax burdens. Here’s what you need to know:

- Key Risks: Probate fees, estate taxes up to 40%, and family disagreements over maintenance or ownership can reduce a property’s value by 25–50% during unplanned transitions.

- Ownership Structures: Options include Tenancy in Common (TIC), LLCs, and Trusts. Each has different implications for liability protection, probate, and management rights.

- Essential Documents: A will, revocable living trust, and LLC operating agreement are critical for defining ownership, avoiding probate, and ensuring smooth management.

- Family Dynamics: Clear communication, usage agreements, and buy-sell provisions help prevent disputes. Professional management services can also reduce family tensions by handling operations impartially.

- Financial Planning: Accurate cash flow forecasts, tax strategies, and maintenance reserves are vital to avoid financial strain on heirs.

Quick Tip: For active rentals, consider an LLC for liability protection and succession control. For family-use properties, trusts can simplify transitions and avoid probate. Always align your legal documents to prevent conflicts.

Want to maximize your property’s value and avoid headaches? Start with a clear plan, involve professionals where needed, and keep family communication open.

How to Put a Vacation Home in a Trust or LLC

sbb-itb-103bddb

Selecting an Ownership Structure for Succession

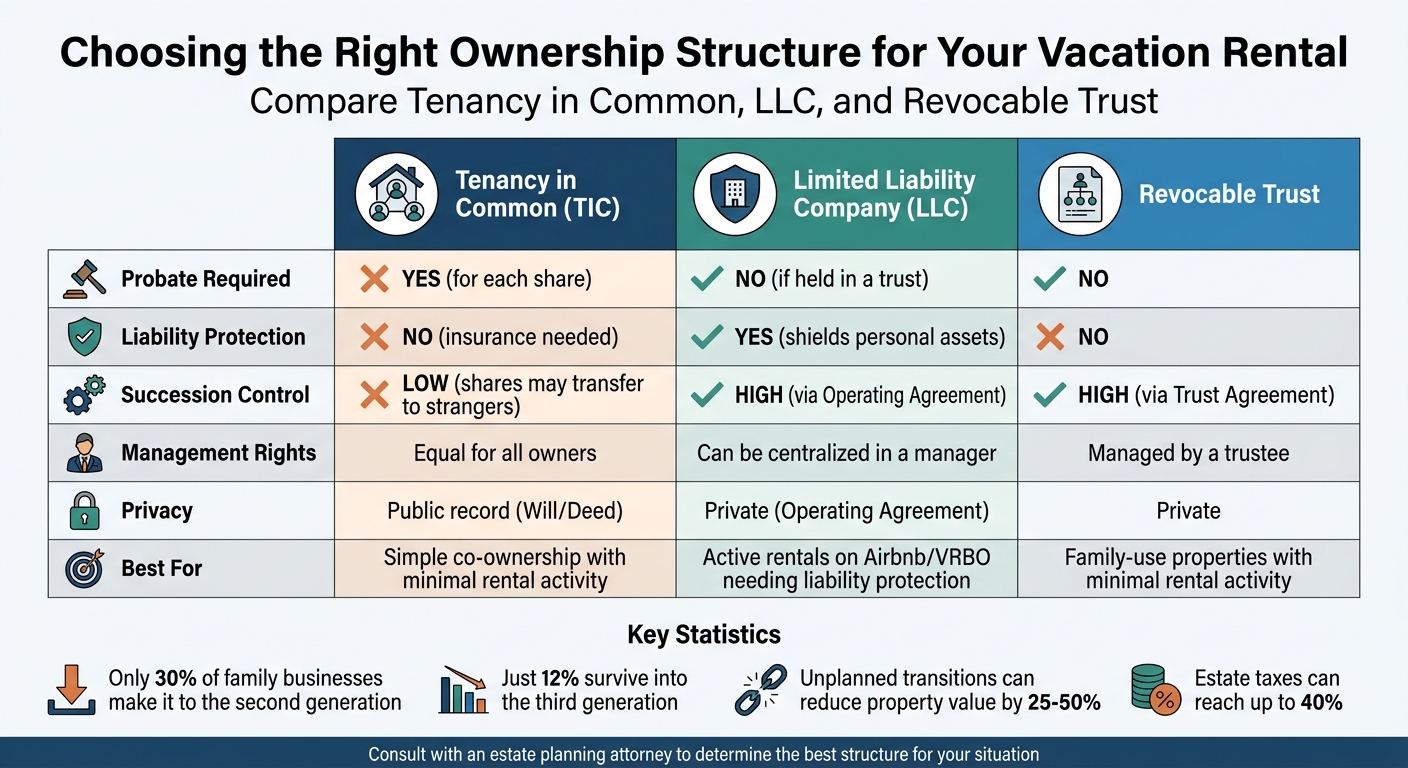

Vacation Rental Ownership Structures Comparison: TIC vs LLC vs Trust

The way you title your vacation rental plays a big role in how smoothly it transfers to the next generation and how much control you retain. Choosing the wrong setup can lead to probate court battles, legal risks, or even leave your heirs powerless to manage a property they technically own. Did you know that only 30% of family businesses make it to the second generation, and a mere 12% survive into the third? [3]. Picking the right structure is key to avoiding these pitfalls and ensuring a seamless transition.

When it comes to structuring ownership, you have three main options: Tenancy in Common (TIC), Limited Liability Companies (LLCs), and Trusts. Each has its own way of handling succession. With TIC, each owner holds a distinct share that passes through a will – often requiring probate [5]. LLCs, on the other hand, transfer ownership through membership interests, which are defined by an operating agreement. This agreement separates "economic rights" (like income) from "management rights" (decision-making power) [3]. Trusts bypass probate entirely by titling the property in the trust’s name, with a successor trustee stepping in immediately if you pass away or become incapacitated [8,10].

Liability protection is another key factor. LLCs shield your personal assets from lawsuits related to rental operations – like if a guest gets injured on your property. TIC and Revocable Trusts don’t offer this protection, so having the right insurance becomes essential.

Tenancy in Common, LLCs, and Trusts: Benefits and Drawbacks

Each structure has its pros and cons when it comes to inheritance and management. Tenancy in Common is straightforward and affordable to set up, but it doesn’t protect against liability and requires probate for every owner’s share [5]. Without a buy-sell agreement, shares could end up with unintended parties after events like a divorce or death [1].

LLCs, meanwhile, offer liability protection and flexible succession planning. For example, you can gift non-voting membership interests to your children while keeping voting control, which also helps reduce your taxable estate. However, if there’s no operating agreement, state laws might leave heirs without management rights. In Arizona, for instance, only the deceased owner’s economic interest transfers to heirs under A.R.S. Title 29. This means heirs can’t vote, force distributions, or sell the property, even though they might still get tax bills from K-1 forms [3].

Revocable Living Trusts are excellent for avoiding probate and keeping matters private since trust documents aren’t part of the public record [9,10]. A successor trustee can step in immediately to manage the property, ensuring continuity. However, trusts don’t protect against liability, and getting a mortgage for a trust-held property can be tricky. For high-value properties, a Qualified Personal Residence Trust (QPRT) can help reduce gift-tax value while letting you retain usage rights for a set period [4].

| Feature | Tenancy in Common | LLC | Trust (Revocable) |

|---|---|---|---|

| Probate Necessitated | Yes, for each share | No (if held in a trust) | No |

| Liability Protection | No (insurance needed) | Yes (shields personal assets) | No |

| Succession Control | Low (shares may transfer to strangers) | High (via Operating Agreement) | High (via Trust Agreement) |

| Management Rights | Equal for all owners | Can be centralized in a manager | Managed by a trustee |

| Privacy | Public record (Will/Deed) | Private (Operating Agreement) | Private |

Understanding these differences helps you weigh your options and choose what’s best for your situation.

How to Choose the Right Structure for Your Property

Start by evaluating your liability exposure. If your property is actively rented on platforms like Airbnb or VRBO, an LLC is often the safest choice to protect your personal assets from potential lawsuits [8,9]. For properties mainly used by family, with little or no rental activity, a Revocable Trust might be sufficient.

Next, think about your family’s dynamics and financial needs. Will your heirs be able to handle ongoing costs like property taxes, insurance, and maintenance? If not, you may need to set up a sub-trust or fund an LLC account to cover those expenses [1,8]. Also, consider dividing responsibilities between "active" heirs (those who will manage the property) and "inactive" heirs. For example, you could leave the rental to active heirs while balancing the inheritance with other assets for the inactive ones [3]. This strategy can help prevent disagreements and forced sales.

For properties with multiple owners, buy-sell agreements are critical. These agreements define who can buy out an owner, at what price, and under what conditions – like divorce, bankruptcy, or simply wanting to sell [1,7]. Without a clear pricing method, disputes are almost inevitable. As RJP Estate Planning puts it:

"A buy-sell that says ‘fair market value’ without a method is a buy-sell that ends up in court" [3].

Lastly, make sure all your legal documents are in sync. Your property deed, LLC operating agreement, and personal will or trust should align to avoid contradictions – a common cause of legal battles after someone passes away [6]. In states like Colorado or Florida, double-check that your chosen structure complies with local probate and tax laws to avoid extra legal hurdles [8,9]. By taking these steps, you can create a solid foundation for your succession plan and ensure a smooth transition for future generations.

Required Estate Planning Documents for Vacation Rentals

Having the right estate planning documents is just as important as choosing the best ownership structure for your vacation rental. These documents ensure a smooth transition of ownership and help avoid unnecessary complications in the future. Once you’ve settled on your ownership structure, gather essential paperwork like property deeds, leases, insurance policies, and mortgage statements before drafting your plan. As estate planning attorney Joseph M. Lento puts it:

"If your family gets along well and you want to keep it that way, then you need to put your instructions in writing and make it absolutely clear how the ownership structure for the family vacation home works in advance of any problems arising" [1].

Key documents for vacation rental owners often include a Last Will and Testament, a Revocable Living Trust, and an LLC Operating Agreement. Each plays a unique role: wills dictate how assets are distributed, trusts help bypass probate and manage incapacity, and operating agreements establish rules for shared ownership. To avoid legal issues, make sure all these documents align. It’s also wise to review and update your estate plan every 2–5 years or after major life changes to keep everything up to date [6].

Creating a Will

A Last Will and Testament is a cornerstone of estate planning. It specifies who inherits your vacation rental and can even name a guardian for minor children. However, wills do have limitations. They go through probate, a lengthy court process that can stretch on for months or years, and they become public record – meaning anyone can see what you owned and who inherited it [6].

If your vacation rental is located in a different state than your primary residence, your heirs might face ancillary probate in that state, adding more time and legal fees. Because of these drawbacks, many property owners treat a will as a backup rather than their main estate planning tool, especially if they also have a trust or LLC in place.

Setting Up a Revocable Living Trust

A Revocable Living Trust is often the preferred option for vacation rental owners who want to avoid probate entirely. By titling the property in the trust’s name, a successor trustee can take over management immediately if you pass away or become incapacitated – no court involvement required [4]. As Kilpatrick Townsend explains:

"Titling your vacation home in your Revocable Trust generally avoids the need to open a probate estate to distribute it because the Trustee will distribute the home to your beneficiaries designated under your trust agreement" [4].

Unlike wills, trusts remain private and can include detailed instructions for managing the property, handling rental income, and covering expenses. For instance, you can create a sub-trust to set aside funds for property taxes, maintenance, and other costs, ensuring these expenses don’t become a burden for heirs with varying financial situations.

Another advantage is flexibility – you can amend a revocable trust at any time during your lifetime to reflect changes in family relationships or property values. However, trusts don’t shield you from liabilities related to rental operations, so it’s essential to maintain proper insurance or consider holding the property in an LLC.

Drafting an Operating Agreement

If your vacation rental is owned through an LLC, the Operating Agreement acts as the rulebook for how the property is managed and passed down. This document outlines who can own shares, how decisions are made, and what happens if a member leaves or passes away. Without a clear agreement, default state laws may kick in, which might not align with your wishes for succession or governance.

A well-crafted operating agreement should include buy-sell provisions that address scenarios like death, divorce, bankruptcy, or retirement. These provisions, along with a clear valuation method, help prevent disputes during significant life events. As LegalGPS explains:

"A well-written succession plan isn’t just about retirement or voluntary sales – it also prepares for sudden events like death, illness, or financial hardships" [7].

Beyond succession planning, the operating agreement should address day-to-day operations. This includes scheduling usage (e.g., who gets priority during holidays), guest policies, pet rules, expense sharing, and rental guidelines. If a family member takes on extra responsibilities – like managing bookings or coordinating with vacation rental managers – the agreement can offer perks, such as first choice on the vacation calendar [1]. To prevent disputes from escalating, consider adding a private arbitration clause to resolve conflicts without forcing the sale of the property [1].

Managing Family Conflicts and Business Operations

After setting up solid legal plans, maintaining open and effective communication is crucial to avoiding family disputes. Even the best estate documents can’t prevent conflicts if there’s a lack of clear communication and operational guidelines. According to Joseph Bierwirth, Jr., a member at Hemenway & Barnes, personal disagreements are the primary cause of forced sales, litigation, and lasting family estrangement – not financial issues [9]. Real estate disputes alone are responsible for family fallout in 9 out of 10 cases, often sparked by a family member’s spouse [1]. Considering that nearly 50% of marriages in the U.S. end in divorce, these disputes can quickly escalate into legal battles that jeopardize the property.

The key to avoiding such conflicts lies in proactive communication and professional management. Regular family governance meetings offer a formal way to discuss finances, share updates, and document decisions in a calm, structured environment [9]. To further reduce tension, establish clear protocols for decision-making. This includes assigning responsibilities for seasonal property upkeep, setting rules for pets and guests, and creating a fair holiday schedule [8]. Using shared online calendars can also help avoid scheduling conflicts and double-bookings.

Holding Family Meetings and Creating Usage Agreements

It’s important to begin succession discussions well in advance – ideally three to five years before the transfer [11]. These early meetings can help identify which heirs are interested in ownership versus those who prefer a buyout. Bringing in a neutral advisor or estate attorney can ensure that everyone’s opinions are heard without the conversation being derailed by family emotions [8][9].

A well-crafted usage agreement is essential, and it should include a tiered dispute resolution process. Start with internal negotiations, move to confidential mediation, and, if necessary, arbitration – reserving litigation as a last resort [9]. The agreement should also address issues like the “handy factor,” where one heir may take on more maintenance work than others. Decide upfront whether extra labor will be compensated with cash, ownership credits, or vacation priority [8][10].

Financial transparency is another critical element. Funding a maintenance endowment through life insurance proceeds or cash reserves can help cover ongoing expenses like taxes, repairs, and utilities [8]. This prevents heirs with limited financial resources from being forced out due to the cost of upkeep. As Bell Wealth Management aptly puts it:

“Common ownership without structure or rules can be a complicated issue to solve without an agreement in place ahead of time” [8].

To further reduce tension and ensure smooth operations, consider bringing in professional management.

Hiring Professional Managers Like Rank One Stays

Professional management companies can eliminate many common sources of family conflict by acting as neutral third parties. For example, a vacation rental management service like Rank One Stays shifts operational decisions away from emotional family dynamics and toward objective, business-focused practices. Tasks like guest services, bookkeeping, and property maintenance – often sources of family resentment – are handled professionally.

Rank One Stays provides a full range of services, including 24/7 guest communication, professional housekeeping coordination, dynamic pricing, and property upkeep. They also offer a transparent owner portal, allowing all family members to stay informed. This professional oversight complements structured family discussions and dispute resolution processes, ensuring a smoother long-term succession plan.

On average, property owners working with Rank One Stays earn 38% more revenue than the market average. This additional income helps cover maintenance, taxes, and operating costs without placing undue financial strain on individual family members. With management fees starting as low as 10% and flexible month-to-month contracts, professional management is an affordable way to prevent family disputes while maximizing property returns. Rank One Stays currently serves property owners in Scottsdale, Arizona; Denver, Colorado; Pittsburgh, Pennsylvania; and Lighthouse Point, Florida.

Financial Planning for Long-Term Success

Once family and operational challenges are addressed, the next step is solid financial planning to secure the property’s future. Smart financial planning can turn a vacation rental from a potential financial strain into a valuable asset. Without proper cash flow projections, heirs may face a property they can’t afford to maintain, leading to costly buyouts or forced sales [12].

Start by identifying your fixed costs (like mortgage payments, property taxes, and insurance) and variable expenses (such as cleaning services, utilities, maintenance, and booking platform fees). A month-by-month cash flow forecast is essential, especially since vacation rentals often experience seasonal revenue swings. By planning for these fluctuations, you can set aside reserves during peak seasons to cover quieter periods or unexpected downturns. Even in a growing market, individual properties still face seasonal cash flow hurdles [12].

Tax planning is another critical piece of the puzzle. For example, under the "21-year rule" for trusts, capital property is considered sold at fair market value every 21 years, which can result in significant capital gains taxes [13]. Additionally, starting in 2026, the federal estate and gift tax exemption will be $13.99 million per individual ($27.98 million for married couples), with amounts above this threshold taxed at a top rate of 40% [15]. As BMO Private Wealth explains:

"If your estate has a shortfall of liquid funds to pay the capital gains tax, you’ll need to consider ways to provide additional funds in your estate for this purpose" [13].

Keep meticulous records of all property renovations and improvements, as these costs can be added to your adjusted cost base (ACB). This reduces the capital gains tax burden when the property is passed on [13]. For vacation rentals, achieving a return on investment (ROI) of 20% to 30% is considered a healthy profit margin when tax obligations are factored in [12].

Projecting Cash Flow and Planning for Taxes

Accurate cash flow forecasting ensures that heirs inherit an asset, not a liability. Without enough liquid funds for maintenance and taxes, families may be pushed into buyouts or sales they can’t afford.

One solution is to establish a maintenance endowment using life insurance proceeds or cash reserves. This can help cover ongoing costs like property taxes, repairs, and utilities. Keeping detailed renovation records can also lower the capital gains tax burden during succession [13]. Anne Cutler, Head of Estate Disposition Advisory at J.P. Morgan, advises:

"The trust agreement can also prevent the house from becoming a financial burden. If you’re able, leave enough money in the trust to pay for the property’s maintenance and repairs" [2].

Dynamic pricing tools can also help maximize revenue by adjusting nightly rates based on local demand and events. This extra income can be directed toward a succession fund [12]. Before transferring the property, it’s wise to conduct a cost-benefit analysis that weighs the hard costs (like repairs and taxes) against the property’s emotional and financial value [2].

Another tax-saving strategy is the step-up in basis at death, which eliminates capital gains tax on appreciation that occurred during the original owner’s lifetime – provided the property transfer is handled correctly [14]. Michael Christy, Regional Vice President of Advanced Planning at Fidelity, notes:

"For tax purposes, you may want to consider allowing the real estate to pass at your death then be sold by your executor or trustee to take advantage of a step-up in basis" [14].

Additionally, you can use the $19,000 annual gift tax exclusion to gradually transfer LLC shares to heirs, reducing the taxable estate while preserving your lifetime exemption [15]. For properties held in LLCs or partnerships, applying discounts for "minority interest" (15–35%) or "lack of marketability" (10–25%) can further lower the taxable value of the transferred interest [15].

Once financial projections and tax strategies are in place, the next step is deciding on the best management approach for long-term success.

Comparing DIY Management and Professional Services

The management model you choose has a direct impact on profitability and ease of succession. Owner-operated models can result in higher profit margins but demand significant time and expertise. On the other hand, professional management offers a more hands-off approach, trading some profitability for scalability and passive income [12].

| Feature | Owner-Operated | Professional Management |

|---|---|---|

| Profit Margin | High (keep all revenue) | Lower (management fees, typically 10%+) |

| Involvement | High (hands-on cleaning and guest communications) | Low (hands-off approach) |

| Revenue Continuity | 3–6 month learning curve during transfer [16] | Immediate cash flow from day one [16] |

| Valuation Premium | Standard market value | 15–25% above market value [16] |

| Documentation | Limited operational data | 2+ years of verified financial data [16] |

Properties with professional management and a documented operational history often sell for a 15–25% premium over comparable properties [16]. For instance, a $1.5 million property could see an additional $225,000 to $375,000 in value [16]. Professional managers also provide audited financials, occupancy records, and forward-booking calendars, all of which are crucial for justifying valuations to heirs or potential buyers [16].

Services like Rank One Stays offer full-service management with fees starting at 10%. They help property owners earn 38% more revenue than the market average. This extra income can cover maintenance, taxes, and operating costs while offering 24/7 guest support, dynamic pricing, professional housekeeping coordination, and a transparent owner portal to keep all heirs informed.

Conclusion

Planning for the future of your vacation rental involves careful attention to four key areas: selecting the right ownership structure, preparing the necessary legal documents, addressing family dynamics, and ensuring financial stability. Without a clear plan, families risk facing disputes, unexpected tax burdens, and operational headaches during transitions.

As Joseph M. Lento, J.D. from Perennial Estate Planning aptly points out:

"The most common reason I’ve seen families fall apart is a disagreement over real estate" [1].

To avoid such conflicts, it’s essential to document your plan thoroughly. This might involve setting up an LLC or trust, creating a revocable living trust to sidestep probate, drafting an operating agreement with clear guidelines for property use and buyouts, and preparing for estate taxes on transfers exceeding the federal exemption [3]. These steps don’t just safeguard the property – they also help maintain family relationships by setting clear expectations.

For operational support, Rank One Stays offers professional management services that simplify running a vacation rental. With management fees starting at 10%, their expertise can boost revenue by 38% above the market average. This additional income can help cover maintenance, taxes, and other expenses while reducing family disagreements over issues like cleaning schedules or renovations.

FAQs

Should I put my vacation rental in an LLC or a trust?

Choosing between an LLC and a trust for your vacation rental comes down to your specific goals and needs.

An LLC is great if you’re looking for liability protection and operational flexibility. It’s especially useful if you plan to manage the property actively or share ownership with others. On the other hand, a trust is more suited for estate planning purposes. It helps avoid probate, simplifies the transfer of ownership, and ensures the property is preserved for future generations.

It’s always a good idea to consult with legal and financial professionals to figure out which option aligns best with your circumstances.

How do I keep heirs from fighting over usage and expenses?

To prevent disagreements among heirs over a vacation rental property, it’s important to set up clear ownership structures and agreements. Legal tools like trusts or co-ownership agreements can outline key details such as usage rights, how expenses will be shared, and procedures for resolving conflicts. Working with an estate planning attorney ensures these arrangements are legally sound and customized to fit your family’s specific situation. This approach helps maintain both family relationships and the property’s worth for generations to come.

What taxes might my heirs owe when inheriting the property?

When heirs inherit property, they may face capital gains taxes. These taxes are typically calculated based on the property’s fair market value at the time of inheritance and any profit made if the property is later sold. Additionally, estate taxes might apply, depending on the total value of the estate and the laws in effect.

To fully understand your tax responsibilities, it’s a good idea to consult a tax professional who can provide guidance tailored to your situation.