When leveraging equity for vacation rentals, choosing between a HELOC (Home Equity Line of Credit) and a cash-out refinance depends on your goals and financial situation. Here’s the quick breakdown:

- HELOC: Works like a credit card secured by your property. You can borrow as needed during a draw period (5–10 years) and pay interest only during that time. Best for short-term needs like renovations or furnishing. Rates are variable (Prime + 1–3% for investment properties), and it doesn’t replace your existing mortgage.

- Cash-Out Refinance: Replaces your current mortgage with a larger one, giving you a lump sum. Ideal for large, one-time expenses like buying a new property or scaling a portfolio. Rates are fixed (7–7.5% for investment properties), ensuring predictable monthly payments.

Key Considerations:

- HELOCs have lower upfront costs but variable rates, making them riskier for long-term debt.

- Cash-out refinancing offers stability with fixed payments but higher closing costs.

- For self-employed investors or those with 10+ properties, a DSCR cash-out refinance qualifies based on rental income rather than personal finances.

Quick Comparison:

| Feature | HELOC | Cash-Out Refinance | DSCR Cash-Out Refi |

|---|---|---|---|

| Loan Type | Second mortgage | Replaces primary mortgage | Replaces primary mortgage |

| Rate Type | Variable | Fixed | Fixed |

| Max LTV/CLTV | 65–75% CLTV | 70–75% LTV | 70–80% LTV |

| Funds Access | Revolving credit line | Lump sum | Lump sum |

| Income Verification | Full documentation | Full documentation | Rental income only |

| Closing Costs | $600–$3,000 (on $120k) | 2–5% of loan amount | 2–5% of loan amount |

| Best For | Renovations, furnishing | Large, one-time expenses | Scaling portfolios |

Bottom Line: If you need flexibility and already have a low mortgage rate, a HELOC may be the better option. For predictable payments and long-term plans, consider a cash-out refinance. Choose based on your goals, current mortgage rate, and how you plan to use the funds.

HELOC vs Cash-Out Refinance for Vacation Rentals: Side-by-Side Comparison

How HELOCs Work for Vacation Rentals

What Is a HELOC and How Does It Work

A HELOC, or home equity line of credit, is a flexible borrowing option secured by your property’s equity. It operates like a credit card: you’re given a credit limit, borrow what you need, pay it back, and can borrow again. Importantly, your primary mortgage remains untouched.

HELOCs typically have two phases: a draw period (usually lasting 5–10 years) where you can borrow as needed and make interest-only payments, and a repayment period (10–20 years) where you pay both principal and interest [6][2].

"You can use and pay back the loan multiple times, as your line of credit will remain open for the entire draw period." – Carol Toren-Edmiston, SVP and Head of Consumer Direct Lending, Flagstar Bank [2]

HELOC rates are variable, often tied to the Prime Rate. As of early 2026, the Prime Rate is around 7.50% [6]. For second homes, rates generally range between 8.25% and 9.00% (Prime + 0.75% to 1.5%). Investment properties, considered riskier by lenders, come with higher rates of Prime + 1.0% to 3.0% [3].

With this foundation, let’s explore what it takes to qualify for a HELOC on vacation rentals.

HELOC Eligibility and Requirements

Getting a HELOC for a vacation rental is more challenging than for a primary residence. Since lenders view vacation rentals as higher risk, the requirements are stricter.

The first factor is how the property is classified. A "second home", where you stay for at least 14 days annually, receives better loan terms compared to a "pure investment property", which is exclusively rented out [6]. The table below highlights the key differences:

| Feature | Second Home HELOC | Investment Property HELOC |

|---|---|---|

| Max CLTV | 75%–85% | 65%–75% |

| Min Credit Score | 680–720 | 700+ |

| Interest Rate | Prime + 0.75%–1.5% | Prime + 1.0%–3.0% |

| Max DTI | 40%–43% | 43%–50% (or DSCR ≥1.0) |

| Closing Speed | 7–30 days | 21–45 days |

Lenders also require 6 to 12 months of PITI reserves (principal, interest, taxes, and insurance) for both your primary and vacation properties [6][8]. A credit score of 740 or higher secures the best rates, but some lenders accept scores as low as 680 if other factors, like strong income or low debt, are favorable. It’s worth noting that only about 15% to 20% of lenders offer HELOCs for non-owner-occupied properties, so comparing options is essential [3].

If you’re an Airbnb or VRBO investor without a long rental history, certain lenders – such as Truss Financial and Griffin Funding – may accept projected rental income or AirDNA data for DSCR (Debt Service Coverage Ratio) calculations instead of traditional income documentation [8][3].

Once approved, a HELOC opens up a range of possibilities for financing vacation rental ventures.

Ways to Use a HELOC for Vacation Rentals

HELOCs are incredibly versatile, making them ideal for various vacation rental strategies. One of the most common uses is funding a down payment on a new property. For example, in March 2026, RefiGuide shared a case where an Austin investor used a $100,000 HELOC from an existing rental to cover a $60,000 down payment on a $300,000 property. This new rental generated $2,500 in monthly rent, yielding a $700 monthly profit after expenses [8].

Another popular use is renovating and furnishing properties to prepare them for short-term rental platforms. In another RefiGuide case, a Miami investor utilized a $50,000 HELOC to fund $40,000 in kitchen and bathroom upgrades. This increased the property’s value from $350,000 to $400,000 and boosted monthly rent by $400, delivering a 96% ROI on the renovation [8].

"A HELOC provides a flexible backstop – draw during slow months, pay it down when rental income is strong." – HonestCasa [6]

However, keep in mind that HELOCs come with variable rates. It’s wise to stress-test your cash flow for potential rate increases of 2% to 3% to ensure your property remains profitable [7]. If you’re furnishing a rental or tackling a design project, the interest-only draw period can ease upfront costs while your property starts generating bookings.

sbb-itb-103bddb

How Cash-Out Refinancing Works for Vacation Rentals

What Is Cash-Out Refinancing and How Does It Work

Cash-out refinancing lets you replace your current mortgage with a larger loan and receive the difference as a lump sum of cash.

"A cash-out refi combines your existing mortgage into a new, larger loan. The money received from it is in one lump sum of cash, so you can take the draw right away." – Dennis Shirshikov, Strategist, Awning.com [2]

Most of these loans come with a fixed interest rate and payments spread over 15 to 30 years, keeping monthly costs consistent. As of 2026, cash-out refinance rates for investment properties generally range from 7% to 7.5%, which is about 0.5% to 1% higher than rates for primary residences [1].

"There is no balloon payment expected after 10 years, which many HELOCs can have. This is why a cash-out refinance is often an option customers find more predictable and easier to manage." – Sean Grzebin, Head of Consumer Originations, Chase Home Lending [2]

Cash-Out Refinancing Eligibility and Requirements

Vacation rental investors can qualify for cash-out refinancing through two main routes: conventional or DSCR loans.

Conventional loans require full income documentation, such as W-2s and tax returns, and are generally for investors with 10 or fewer financed properties. Loan-to-value (LTV) ratios are capped at 70% to 75% for single-unit properties and 65% to 70% for properties with 2–4 units [3]. A credit score of at least 680 is usually necessary.

DSCR loans (Debt Service Coverage Ratio) are better suited for self-employed investors or those with complex income streams. Instead of evaluating personal finances, lenders focus on whether the rental income can cover the mortgage payment, typically requiring a coverage ratio of 1.0 to 1.25 times PITIA (Principal, Interest, Taxes, Insurance, and Association fees) [3]. These loans allow up to 80% LTV, accept credit scores as low as 660, and have no limit on the number of properties owned. DSCR loans also tend to have shorter seasoning periods compared to conventional loans.

"DSCR lenders evaluate the deal, not the borrower’s personal finances. I’ve closed DSCR cash-out loans for investors holding 30+ properties in an LLC – borrowers who would never qualify conventionally." – Mo Abdel, Mortgage Broker [3]

| Feature | Conventional Cash-Out | DSCR Cash-Out Refi |

|---|---|---|

| Qualification | W-2 income / Tax returns | Rental income (DSCR ratio) |

| Max LTV (1-unit) | 70%–75% | 70%–80% |

| Min Credit Score | 680+ | 660–680+ |

| Seasoning | 6–12 months | 3–6 months |

| Property Limit | Up to 10 financed | No limit |

Both options require 6 to 12 months of cash reserves for the refinanced property, along with reserves for other owned properties [1]. Closing costs typically range from 2% to 5% of the loan amount. For example, on a $400,000 loan, you’d pay between $8,000 and $20,000 in closing fees, depending on the loan type [3].

Ways to Use Cash-Out Refinancing for Vacation Rentals

Cash-out refinancing provides immediate funds, making it ideal for large, up-front investments. Unlike HELOCs, which offer flexibility over time, the lump-sum structure of cash-out refinancing is perfect for significant one-time expenses like:

- Funding a down payment on a new property

- Financing major renovations

- Furnishing a rental property from scratch

For those setting up a turnkey rental, having a fixed budget upfront simplifies planning, especially when working with professional vacation rental interior design and staging.

Cash-out refinancing also plays a key role in the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat). Once a property is generating rental income, investors can refinance to recover their initial investment and use it for their next project. For those using DSCR loans, starting the refinance application around month four of ownership ensures the process is completed once seasoning requirements are met [3].

Another benefit: interest on cash-out proceeds used for property-related expenses is typically tax-deductible as a business expense on Schedule E. However, the IRS applies interest tracing rules, so maintaining clear records of how the funds are spent is essential [3].

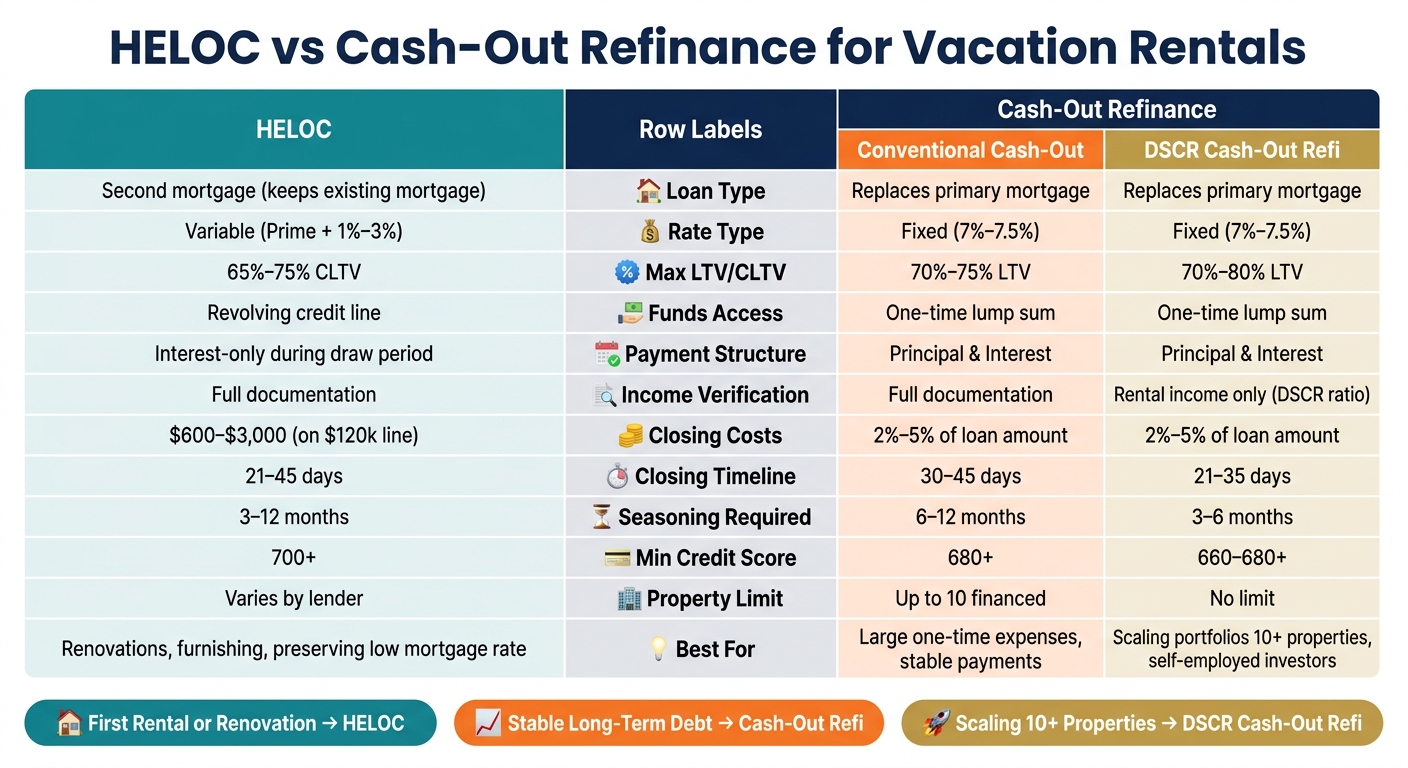

HELOCs vs. Cash-Out Refinancing: A Side-by-Side Comparison

Key Factors to Compare

When deciding between a HELOC and cash-out refinancing for your vacation rental, it’s important to understand how each impacts your mortgage and overall costs.

The main distinction lies in how these options interact with your existing mortgage. With a cash-out refinance, your current mortgage is replaced entirely with a new, larger loan at today’s interest rates. In contrast, a HELOC acts as a second mortgage, leaving your original loan – and its rate – untouched [2]. If current rates exceed 7%, refinancing could mean paying that higher rate on your entire loan balance, not just the equity you withdraw, which may increase your long-term expenses.

"If refinancing would increase your rate on the full balance, a HELOC is almost always the better choice." – Dennis Shirshikov, Strategist, Awning.com [2]

Upfront costs also vary significantly. Cash-out refinancing typically involves closing costs of 2% to 5% of the total loan amount. For example, on a $400,000 loan, you’d pay between $8,000 and $16,000. HELOCs, on the other hand, have lower closing costs – usually 0.5% to 2% of the credit line, which translates to $600 to $3,000 for a $120,000 line. For short-term needs, like furnishing a rental property over 12 to 18 months, the lower upfront costs of a HELOC can be appealing, even with its variable interest rate [3].

Predictability in cash flow is another key consideration. Cash-out refinancing provides fixed monthly payments, which can simplify budgeting for vacation rentals that experience seasonal income fluctuations. In contrast, HELOCs often come with variable rates (Prime plus 1% to 3% for investment properties), which can lead to fluctuating payments. Once the interest-only draw period ends – usually after 5 to 10 years – payments can increase significantly as the loan transitions to full amortization [2] [4]. For investors who are self-employed or own more than 10 financed properties, DSCR cash-out refinancing offers added flexibility by qualifying the loan based on rental income instead of personal income – a feature HELOCs typically lack [3].

The table below outlines the differences between these options at a glance.

Comparison Table: HELOCs vs. Cash-Out Refinancing

| Feature | Investment HELOC | Conventional Cash-Out | DSCR Cash-Out Refi |

|---|---|---|---|

| Loan Position | Second mortgage | Replaces primary | Replaces primary |

| Rate Type | Variable (Prime + 1%–3%) | Fixed | Fixed |

| Max LTV/CLTV | 65%–75% CLTV | 70%–75% LTV | 70%–80% LTV |

| Funds Access | Revolving credit line | One-time lump sum | One-time lump sum |

| Payment Structure | Interest-only (draw period) | Principal & Interest | Principal & Interest |

| Income Verification | Full documentation | Full documentation | Rental income only |

| Closing Costs | $600–$3,000 (on $120k line) | 2%–5% of total loan | 2%–5% of total loan |

| Closing Timeline | 21–45 days | 30–45 days | 21–35 days |

| Seasoning Required | 3–12 months | 6–12 months | 3–6 months |

| Property Limit | Varies by lender | Up to 10 financed | No limit |

HELOCs can be harder to secure due to limited lender availability, while cash-out refinancing – especially DSCR options – tends to be more accessible for vacation rental investors. Understanding these differences can help you choose the financing option that best fits your investment strategy.

Cash-Out Refinance vs. HELOC | Watch Before You Choose

Choosing the Right Financing Option for Your Vacation Rental Goals

Once you’ve covered the basics of financing, the next step is selecting the option that aligns with your vacation rental goals. Factors like your current mortgage rate, how you plan to use the funds, and the number of properties you own can all help point you in the right direction. Your investment stage also plays a key role in determining the best financing tool.

Funding Your First Vacation Rental

If you’re tapping into the equity in your primary residence to fund your first vacation rental, a HELOC (Home Equity Line of Credit) is often the better choice – especially if you locked in a low mortgage rate (3% to 4%) during 2020 or 2021. Why? A cash-out refinance would replace your existing mortgage with a new loan at today’s higher rates, meaning you’d pay more on your entire balance. A HELOC, on the other hand, leaves your original mortgage untouched and is typically much cheaper to set up [3][2].

As your investment goals grow, your financing needs will likely evolve too.

Growing a Portfolio with Existing Equity

When you’re ready to scale your vacation rental portfolio, a DSCR (Debt-Service Coverage Ratio) cash-out refinance can be a game-changer. Conventional cash-out refinancing comes with limits – like capping borrowers at 10 financed properties and requiring full W-2 income documentation. These restrictions can be a major hurdle for self-employed investors or those with larger portfolios.

DSCR cash-out refinancing sidesteps these barriers by qualifying based on rental income rather than personal finances. Plus, it allows you to access equity after just 3–6 months, making it ideal for investors looking to expand beyond 10 properties [3][1].

"DSCR lenders evaluate the deal, not the borrower’s personal finances… the ability to qualify on rental income alone removes the bottleneck [for scaling]." – Mo Abdel, NMLS #1426884 [3]

Renovating or Furnishing a Vacation Rental

Financing doesn’t stop at acquiring a property – it also plays a role in making upgrades. For renovations, a HELOC is often the most practical option. Renovation costs are rarely set in stone, and a HELOC’s revolving structure lets you draw only what you need. For example, if you’re spending $50,000 on a kitchen remodel, you’ll only pay interest on that amount – not on a larger lump sum sitting in your account. During the draw period, payments are interest-only, keeping your monthly costs low while the property is being upgraded and isn’t generating full rental income yet [3].

If your goal is to enhance your rental’s appeal – like investing in furniture, professional photography, or landscaping to boost nightly rates – a HELOC can help you spread out spending across different phases without borrowing more than necessary.

Protecting Cash Flow During Market Swings

Vacation rentals often experience seasonal demand, and market shifts can affect booking rates. A fixed-rate cash-out refinance offers stability by locking in predictable monthly payments. This makes it easier to manage cash flow during slower seasons. In contrast, a HELOC’s variable rate (usually Prime plus 1% to 3% for investment properties) could increase your payments just as rental income dips – a risky combination, even for well-performing properties [3][2]. For long-term holds of five years or more, a fixed-rate cash-out refinance is the safer choice if rate stability matters more than flexibility.

Here’s a quick summary to match your goals with the right financing option:

| Investor Goal | Best Option | Why It Works |

|---|---|---|

| Fund first rental | HELOC on primary residence | Preserves low rate and minimizes costs [3][2] |

| Scale beyond 10 properties | DSCR cash-out refinance | Qualifies on rental income; no property count limits [3] |

| Renovate or furnish | Investment HELOC | Interest-only draws match phased rehab timelines [3] |

| Stable, predictable payments | Cash-out refinance | Fixed rate simplifies long-term cash flow planning [3][2] |

| Recycle capital quickly | DSCR cash-out refinance | Shorter seasoning period of 3–6 months [3][1] |

How Professional Management Helps Investors Using Leverage

Why Management Quality Matters for Leveraged Properties

Owning a leveraged property comes with its challenges. Every month a property underperforms, you’re stuck paying interest without enough income to cover expenses. That’s a fast track to shrinking profit margins. The situation gets even worse when factors like vacancies, rising maintenance costs, or variable-rate loans pile on. As one financial expert put it:

"The best home-equity deals are not the ones where the investor barely gets over the finish line. They are the ones where the equity tool improves flexibility while the deal still works cleanly on its own numbers." – Doorvest [9]

This is where professional management steps in. By focusing on things like maximizing listing visibility, competitive pricing, and high occupancy rates, expert management ensures the property earns what the market can support. Companies like Rank One Stays specialize in this, making them a key partner for investors navigating leverage.

How Rank One Stays Supports Leveraged Investors

Rank One Stays offers a full-service vacation rental management solution tailored for investors who rely on their properties to perform. With management fees starting at just 10% of rental income – an expense that’s often tax-deductible – Rank One Stays helps offset the interest costs tied to HELOCs or cash-out refinances [5][11]. On average, properties under their management generate 38% more revenue than the market norm, giving investors a significant edge when it comes to servicing leverage.

Their approach is all about optimizing operations after financing. This includes services like dynamic pricing, optimizing Airbnb and VRBO listings, 24/7 guest support, professional cleaning, and managing damage claims. If you’ve used HELOC or cash-out funds for property renovations, Rank One Stays can also help with vacation rental interior design and staging, transforming your property into a ready-to-rent, income-generating asset.

Rank One Stays operates in high-demand markets like Scottsdale, Arizona, Denver, Colorado, Pittsburgh, Pennsylvania, and Lighthouse Point, Florida. These locations combine strong short-term rental demand with the company’s expertise in property optimization.

Pairing Financing with Professional Management

Choosing the right financing – whether a HELOC or cash-out refinance – is just the first step. The real challenge begins after closing, where the property’s performance determines its success. Without strong management, poor occupancy rates and ineffective pricing can quickly turn an asset into a liability.

"With great management, the property will yield income for years." – Tim Lucas, Licensed Loan Originator [12]

Professional management doesn’t just stabilize revenue; it also simplifies daily operations and builds a rental income history. This documented performance can be a game-changer when it’s time to refinance, as many DSCR lenders require proof of consistent income. Combining smart financing with expert management gives investors the tools to scale their portfolios instead of hitting roadblocks.

Conclusion: Picking the Right Financing Path for Your Vacation Rental

Choosing the right financing option comes down to your specific circumstances. If you locked in a low-rate mortgage in the past, a HELOC could be your best bet. On the other hand, if your current mortgage rate is above 6%, opting for a cash-out refinance might save you money on borrowing costs while providing a lump sum for your needs [7]. The key is to ensure your choice aligns with your financial goals and cash flow strategy.

The structure of your project matters just as much as the interest rate. A HELOC works well for phased spending, like staggered renovations, since you only pay interest on the amount you draw. Meanwhile, a cash-out refinance is better suited for significant, one-time expenses, like purchasing a new property. For short-term needs, a HELOC is often cheaper to set up, but if you plan to hold the debt for five years or more, a fixed-rate cash-out refinance can help you save on total interest [3]. If you’re managing a portfolio of more than 10 properties or have complex tax returns, a DSCR cash-out refinance could be advantageous, as it allows qualification based solely on rental income [3]. To get the best results, combining these financing tools with dependable management is crucial.

Bhavesh Patel, Head of Field Sales at Chase Home Lending, highlights the advantage of HELOCs in certain situations:

"If a homeowner is sitting at a lower rate, a HELOC might be a better option because it allows you to borrow against your home’s equity without changing the terms of your existing mortgage." [10]

No matter which financing route you take, generating strong income is vital to manage debt obligations effectively. This is where professional vacation rental management becomes a game-changer – turning your financed property into a consistent, cash-flowing asset instead of a financial burden. For expert support in managing your vacation rental investment, take a look at the services offered by professional vacation rental management.

FAQs

How do I decide between a HELOC and a cash-out refinance if I already have a low mortgage rate?

If you have a low mortgage rate, a HELOC might be a smarter choice since it allows you to tap into your home’s equity without refinancing into a higher-rate mortgage. HELOCs provide flexible, revolving credit and typically come with variable interest rates. On the other hand, a cash-out refinance replaces your current mortgage with a larger loan at today’s rates, which could lead to higher monthly payments. Your decision should depend on your existing mortgage rate, whether you need flexible funding, and your long-term financial goals.

What happens to my payments when a HELOC draw period ends?

When the draw period of your HELOC ends, you move into the repayment phase. At this stage, you’ll begin paying back the money you borrowed. Early on, your payments might only cover the interest. However, over time, they will include both the interest and the principal. The repayment phase can extend for as long as 20 years, depending on the terms of your loan.

When does a DSCR cash-out refinance make more sense than a conventional cash-out refinance?

A DSCR (Debt Service Coverage Ratio) cash-out refinance is a great option if you prefer to qualify using rental income instead of personal income. This type of loan is particularly appealing for investors who have solid rental income but lack extensive W-2 or personal income documentation. One of the key benefits of DSCR loans is that they typically allow higher loan-to-value (LTV) ratios – often between 70% and 80%. This gives you the ability to tap into more of your property’s equity while still securing favorable terms.